- AQH Weekly Deep Dive

- Posts

- The Quant Edge: How Quants Design Algo Trading Strategies in Credit Markets

The Quant Edge: How Quants Design Algo Trading Strategies in Credit Markets

AlgoQuantHub Weekly Deep Dive

Nicholas Burgess

February 20, 2026

Welcome to the Deep Dive!

Here each week on ‘The Deep Dive’ we take a close look at cutting-edge topics on algo trading and quant research.

This Week, we dive into algo trading in credit markets and discuss how Quants design low latency pricing and risk analytics to support live algorithmic trading.

Bonus Content, we present a case study showing how to design an algo trading strategy for credit markets, where we use statistical arbitrage and pairs-trading techniques to build a relative value correlation dispersion trading strategy, leveraging the pricing and risk analytics from our feature article.

Table of Contents

Feature Article: How Quants Design Low Latency Pricing and Risk Analytics in Credit Markets

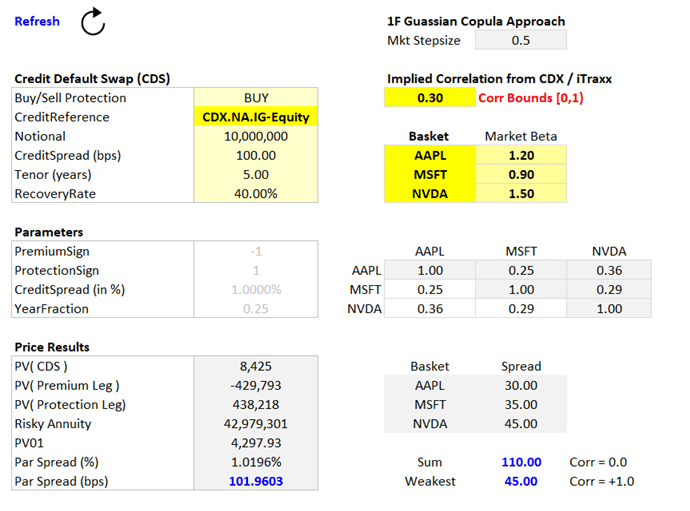

A first-to-default CDS (FTD) is a credit derivative that pays a protection or insurance-like contingent payment when the first credit default occurs with reference to a basket of corporate bonds. The FTD price is primarily driven by market implied correlation, see Credit Correlation Trading with First-to-Default CDS.

A correlation of 0 implies defaults are independent, so the FTD spread will roughly equal the highest single-name CDS spread in the basket—the “weakest link.”

A correlation of 1 implies the names default together every time, so the FTD spread approaches the sum of all single-name CDS spreads, as if the basket were a single risky entity.

First-to-Default CDS

Pricing a FTD basket is fundamentally about modelling joint default risk. Unlike a single-name CDS, where valuation depends on one hazard curve and discount curve, the FTD payoff depends on the earliest default time across multiple names. That immediately forces us to move from marginal default probabilities to a full dependence structure.

In practice, the Quant workflow starts with three calibration building blocks (i) an interest rate yield curve for discounting, (ii) single-name hazard rate curves bootstrapped from CDS spreads, and (iii) a validated single-name CDS pricer to ensure curve consistency.

The core modelling challenge is correlation, see Exotic Credit Trading and Implied Correlation Surfaces. The industry standard remains the one-factor Gaussian copula, where correlated default times are generated by mapping correlated normal variables into survival probabilities. Intuitively, each firm’s asset return is decomposed into a systemic factor and an idiosyncratic component; the loading on the systemic factor determines implied correlation. The dependence structure can be summarised as:

where M is the common market factor, ϵi are independent shocks, and ρ is the asset correlation parameter inferred from market prices. This structure allows us to translate calibrated hazard curves into joint default probabilities for the basket.

From here, pricing can follow two routes. An analytical approach integrates over the common factor distribution to compute the probability that the first default occurs before maturity, typically via numerical integration. Alternatively, a Monte Carlo framework simulates correlated default times directly. In practice, efficiency techniques are essential: low-discrepancy sequences e.g. Sobol Brownian Bridge to improve convergence, while importance sampling deliberately over-weights default and tail scenarios to stabilise protection leg PV estimates. Without these variance-reduction tools, simulation counts become impractically large.

The final output is the present value of premium and protection legs, consistent with single-name calibration and an implied correlation parameter. At this point, the model is not just a pricing engine — it becomes a risk engine. Sensitivities such as correlation delta emerge naturally, enabling systematic positioning, and modern implementations increasingly rely on Algorithmic Adjoint Differentiation (AAD), training machine learning algorithms and neural networks, to accelerate real-time pricing and risk calculations.

With low latency pricing and risk analytics in place, Quants proceed to the set-up of algo trading strategies, signal generation, back-testing and live trading preparation as illustrated in the bonus article.

Keywords: first-to-default CDS, CDX, iTraxx, implied correlation, basket CDS, Gaussian copula, correlation trading, pricing, numerical integration, Monte Carlo, Sobol, AAD, machine learning, neutral networks, real-time, low latency, risk.

Recommended Reading:

Bonus Article: How Quants Design Algo Trading Strategies in Credit Markets

Using Statistical Arbitrage to Build a Correlation Dispersion Trading Strategy

A naïve approach would be to simply buy FTD when correlation is low and sell it when correlation is high. The problem is that an outright FTD position carries significant exposure to credit spreads, systemic shocks, and jump-to-default risk. What we want instead is a pure correlation trade — one that is largely market-neutral, not directional in credit risk.

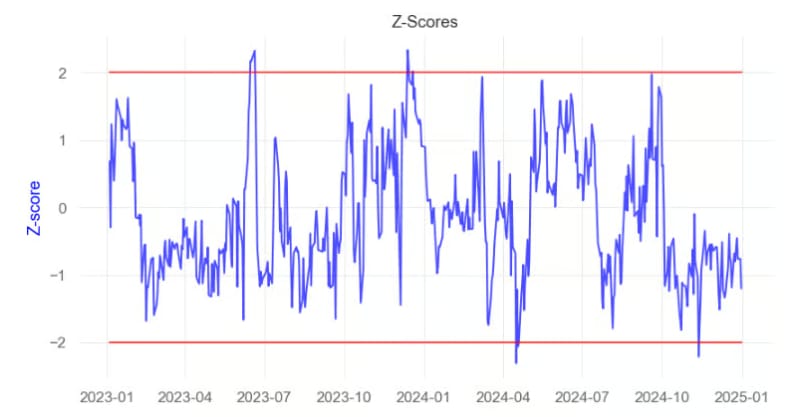

The strategy therefore uses statistical arbitrage and pairs-trading techniques to treat implied correlation as a relative-value spread. Step one is to imply correlation from CDX index equity tranches by inverting the tranche pricing model, where the 1 factor Gaussian copula approach is the standard pricing approach. This produces a daily time series ρ(t). We then compute a rolling mean and standard deviation to standardise deviations:

Z( t ) = ( ρ( t ) − μ( t ) ) / σ( t )

This z-score is our trading signal. We monitor it for mean reversion, optionally test for stationarity, and estimate the half-life using an Ornstein–Uhlenbeck regression to calibrate expected holding periods.

Z-Score Illustration

Execution is threshold-based, typically at ±2 standard deviations.

If z( t )<−2, correlation is statistically cheap. We buy FTD protection and sell single-name CDS protection, sized using correlation delta.

If z( t )>+2, correlation is statistically rich. We sell FTD protection and buy single-name CDS protection, again sized via correlation delta.

Correlation delta ensures that the single-name hedge offsets first-order spread risk, leaving the portfolio primarily exposed to changes in implied correlation. In effect, this transforms the position into a dispersion-style pairs trade between basket-level dependence and individual credit risk. Rebalancing should be rule-driven and backtests must include transaction costs and turnover constraints, as multiple CDS legs can amplify trading frequency.

The full pipeline is precise and mechanical: imply correlation from equity tranche → build time series → compute rolling z-score → assess mean-reversion and half-life → apply ±2σ thresholds → size positions via correlation delta → monitor convergence and P&L attribution.

The result is not a directional bet on credit, but a structured attempt to monetise temporary dislocations in how markets price dependence itself. All trades are backtested and simulated first, executed with small positions initially, and risk limits are gradually increased as the strategy proves robust.

Video Lecture Series

Hudson and Thames provide an excellent video series introduction to pairs trading strategies, click-here for more details. Note video links are at the bottom.

Keywords

Correlation Trading, Exotic Credit, Algorithmic Trading, Statistical Arbitrage, Pairs Trading, Trading Strategy, Backtesting

Algo Quant YouTube Channel

Algo Trading & Quant Research Channel

YouTube playlists include:

Interest Rate Markets

Bond Markets

Credit Derivatives

Monte Carlo Simulation

Advanced Quant Models

American Option Trading

Live Algo Trading with IB Broker

Exclusive Algo Quant Store Discounts

Algo Trading & Quant Research Hub

Get 25% off all purchases at the Algo Quant Store with code 3NBN75MFEA.

Useful Links

Quant Research

SSRN Research Papers - https://ssrn.com/author=1728976

GitHub Quant Research - https://github.com/nburgessx/QuantResearch

Learn about Financial Markets

Subscribe to my Quant YouTube Channel - https://youtube.com/@AlgoQuantHub

Quant Training & Software - https://payhip.com/AlgoQuantHub

Follow me on Linked-In - https://www.linkedin.com/in/nburgessx/

Explore my Quant Website - https://nicholasburgess.co.uk/

My Quant Book, Low Latency IR Markets - https://github.com/nburgessx/SwapsBook

AlgoQuantHub Newsletters

The Edge

The ‘AQH Weekly Edge’ newsletter for cutting edge algo trading and quant research.

https://bit.ly/AlgoQuantHubEdge

The Deep Dive

Dive deeper into the world of algo trading and quant research with a focus on getting things done for real, includes video content, digital downloads, courses and more.

https://bit.ly/AlgoQuantHubDeepDive

|  |

Feedback & Requests

I’d love your feedback to help shape future content to best serve your needs. You can reach me at [email protected]