- AQH Weekly Deep Dive

- Posts

- Surviving the Drawdown – Trading and Risk Management in Chaotic Markets

Surviving the Drawdown – Trading and Risk Management in Chaotic Markets

AlgoQuantHub Weekly Deep Dive

Nicholas Burgess

March 13, 2026

Welcome to the Deep Dive!

Each week on The Deep Dive we explore cutting-edge ideas in algorithmic trading, quantitative research, and modern financial engineering.

This week’s Deep Dive we explore why drawdowns accelerate when markets become non-linear, and how traders and investors can prepare for these regime shifts. We discuss how professional portfolio managers navigate drawdowns and market chaos.

Bonus content, in theory, surviving non-linear markets sounds straightforward: control risk, maintain diversification, and stay disciplined. In practice, portfolio managers rely on a set of concrete tools—from systematic rebalancing to options and credit hedges—to navigate drawdowns without being forced out of positions.

Table of Contents

Feature Article:

Surviving the Drawdown – Risk Management When Markets Go Non-Linear

Financial markets often appear predictable during calm periods. Risk models assume that returns follow familiar distributions, correlations remain relatively stable, and small shocks lead to proportionally small price movements. This is what we might call a linear market environment. In such regimes, diversification works as expected: equities fall and bonds often rally, commodities respond to growth expectations, and portfolio volatility remains manageable. Most portfolio construction frameworks—from Value-at-Risk models to historical Monte Carlo simulations—implicitly assume that these relationships remain stable.

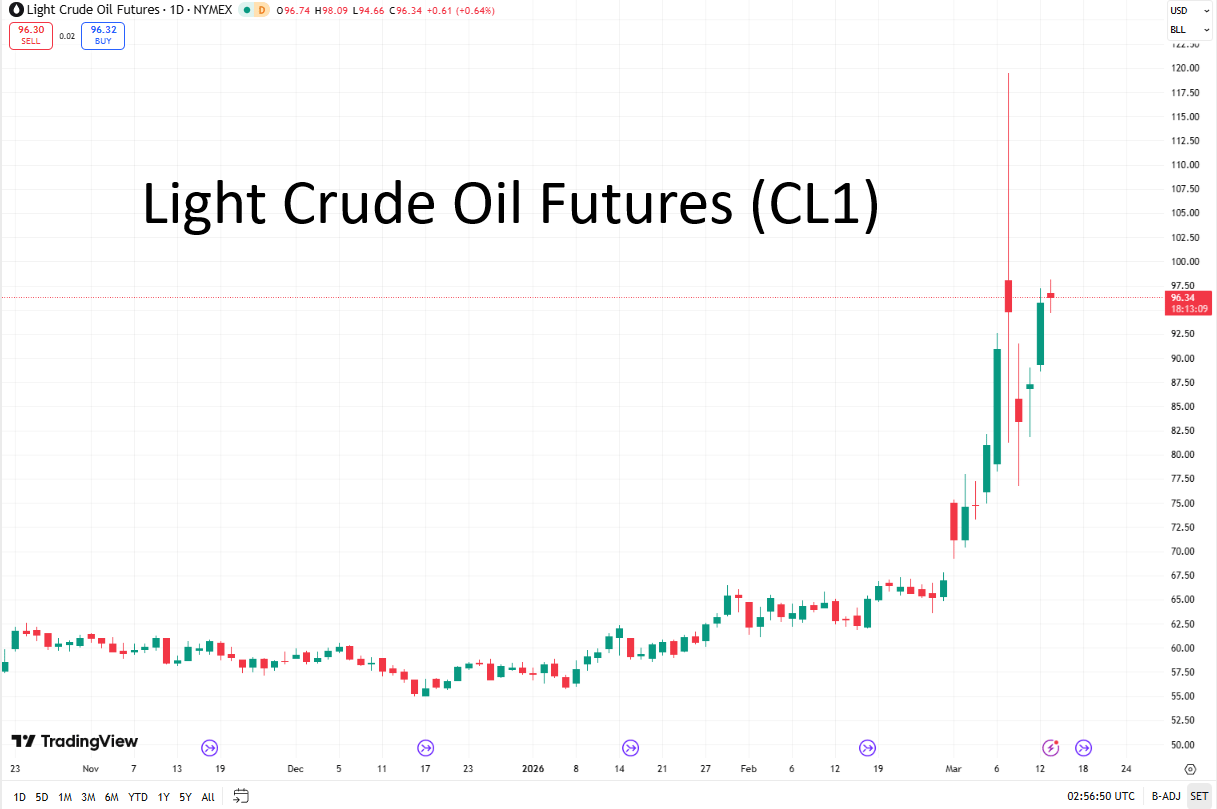

Recent geopolitical tensions and conflict escalation in the Middle East have shown how quickly that assumption can break down. Oil prices have surged on supply fears, inflation expectations have moved higher, and bond yields have reacted sharply. The result has been an unusual environment where equities, bonds and even gold have experienced drawdowns at the same time. In these regimes markets behave in a non-linear way, meaning small shocks can trigger disproportionately large moves. Liquidity thins, volatility rises sharply, and correlations between assets begin to move toward one. In options terminology, the system develops convexity or “gamma”, where price moves accelerate as stress spreads through the market.

This is why drawdowns tend to accelerate during crises. The danger is not simply volatility, but structural shifts in market behaviour. Diversification temporarily fails, forced positioning dominates price action, and risk models based on historical data become unreliable. Professional portfolio managers focus less on predicting these events and more on surviving them. That means controlling position sizes, maintaining liquidity buffers, avoiding excessive leverage, and structuring portfolios so they can withstand temporary dislocations without forced liquidation. Drawdowns are inevitable, but portfolios designed to survive non-linear regimes are the ones that remain positioned to benefit when stability eventually returns.

Keywords:

drawdowns, non-linear markets, convexity, gamma, regime shifts, portfolio risk, diversification breakdown, correlations, liquidity risk, geopolitical shocks, volatility regimes, portfolio resilience

Recommended Reading:

Taleb, N. N. – The Black Swan

Taleb, N. N. – Dynamic Hedging

Mandelbrot, B. – The Misbehavior of Markets

Meucci, A. – Risk and Asset Allocation

Ang, A. – Asset Management: A Systematic Approach to Factor Investing

Bonus Article:

Implementing Resilient Risk Management in Practice

Understanding non-linear markets is one thing; managing portfolios through them is another. Professional investors use a combination of structural portfolio design and active risk management. Long-horizon investors often remain invested during drawdowns but rely on disciplined portfolio sleeve rebalancing to maintain allocation targets. For example, a portfolio designed to hold 60% equities and 40% bonds will periodically rebalance back to those weights as market moves push allocations away from their targets. This process does not involve abandoning winning assets for losers, but simply maintaining the intended portfolio structure while systematically buying during dips and trimming positions after rallies - this is called volatility harvesting.

Other strategies focus more directly on protecting capital during stress regimes. Traders may reduce position sizes early when drawdowns begin, purchase put options to provide convex downside protection, or hedge systemic risk using instruments such as credit default swap indices. Some long-term investors take advantage of elevated volatility by selling put options on assets they are happy to own at lower prices, allowing them to collect volatility premiums while potentially acquiring assets at discounted levels. Alongside these techniques, many risk systems now complement traditional Value-at-Risk (VaR) metrics with Expected Shortfall, which better captures the magnitude of extreme losses once tail events occur.

Modern trading infrastructure makes these approaches increasingly practical. Real-time market data, broker APIs, and quantitative risk frameworks allow investors to continuously monitor exposures, run stress scenarios, and identify hidden concentrations of risk across a portfolio. The goal is not to eliminate drawdowns entirely—an impossible task—but to build portfolios resilient enough to survive non-linear market regimes and remain positioned when the next opportunity emerges.

Keywords:

Risk management implementation, stress testing, Monte Carlo simulation, Expected Shortfall, VaR, portfolio rebalancing, volatility strategies, credit hedging, trading infrastructure, portfolio monitoring

Algo Quant YouTube Channel

Algo Trading & Quant Research Channel YouTube playlists include:

Interest Rate Markets

Bond Markets

Credit Derivatives

Monte Carlo Simulation

Advanced Quant Models

American Option Trading

Live Algo Trading with IB Broker

Useful Links

Quant Research

SSRN Research Papers - https://ssrn.com/author=1728976

GitHub Quant Research - https://github.com/nburgessx/QuantResearch

Learn about Financial Markets

Subscribe to my Quant YouTube Channel - https://youtube.com/@AlgoQuantHub

Quant Training & Software - https://payhip.com/AlgoQuantHub

Follow me on Linked-In - https://www.linkedin.com/in/nburgessx/

Explore my Quant Website - https://nicholasburgess.co.uk/

My Quant Book, Low Latency IR Markets - https://github.com/nburgessx/SwapsBook

AlgoQuantHub Newsletters

The Edge

The ‘AQH Weekly Edge’ newsletter for cutting edge algo trading and quant research.

https://bit.ly/AlgoQuantHubEdge

The Deep Dive

Dive deeper into the world of algo trading and quant research with a focus on getting things done for real, includes video content, digital downloads, courses and more.

https://bit.ly/AlgoQuantHubDeepDive

|  |

Feedback & Requests

I’d love your feedback to help shape future content to best serve your needs. You can reach me at [email protected]