- AQH Weekly Deep Dive

- Posts

- Advanced Portfolio Management: Harvesting Volatility & Exploiting Convexity for Superior Long-Term Returns

Advanced Portfolio Management: Harvesting Volatility & Exploiting Convexity for Superior Long-Term Returns

AlgoQuantHub Weekly Deep Dive

Nicholas Burgess

January 30, 2026

Welcome to the Deep Dive!

Here each week on ‘The Deep Dive’ we take a close look at cutting-edge topics on algo trading and quant research.

This Week, discover how disciplined rebalancing leverages convexity and correlation to systematically harvest volatility, turning market fluctuations into superior long-term portfolio growth.

Bonus Content, see volatility harvesting in action through a real-world portfolio example, illustrating how systematic rebalancing converts market movements into incremental gains and higher compounded returns.

All materials are for informational purposes only and do not constitute investment advice. Figures are illustrative and intended to demonstrate structural effects rather than forecast performance.

Table of Contents

Feature Article: Volatility Harvesting: Exploiting Convexity and Correlation for Superior Growth

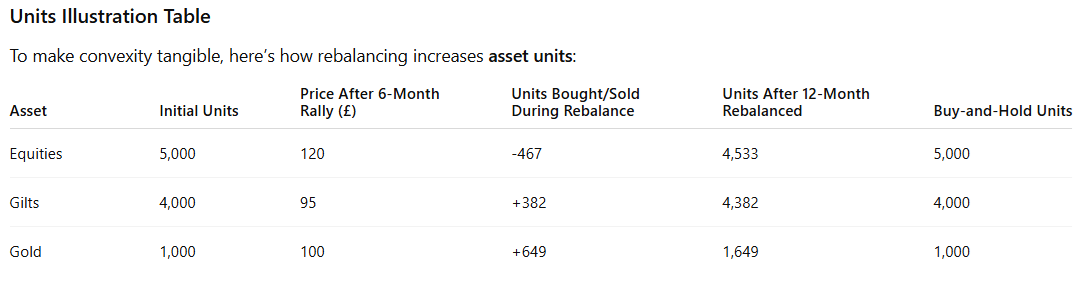

Traditional portfolio management focuses on expected returns. Modern portfolio management focuses on paths. This distinction matters because investors do not experience averages — they experience sequences of gains and losses. Volatility harvesting emerges from this reality. When assets fluctuate and are periodically rebalanced, the portfolio’s response becomes nonlinear. Rebalancing systematically sells assets after strength and buys after weakness, creating a payoff that benefits from variance itself.

Consider a simple illustration: an asset drops 20% from £100 to £80, then rises 25% back to £100. If you buy more when the price drops and sell when it rises, you end up with more units of the asset than you started with. Over time, this “extra unit accumulation” compounds, even though the asset’s expected return is unchanged. This is convexity: the portfolio gains more from volatility than it loses, purely from disciplined interaction with movement.

Volatility harvesting can also be viewed as a form of pairs trading. In the ETF or macro sleeves, relative movements between assets — for example equities vs. bonds, or GBP vs. USD exposures — create temporary mispricing. Rebalancing acts like a pairs trade: selling the relatively rich asset and buying the relatively cheap one. Mean-reversion is not required in the underlying asset prices themselves, but it underpins the relative value between components, creating incremental growth over repeated cycles. This insight ties volatility harvesting to both macro allocation and tactical rebalancing disciplines.

Correlation is the silent partner in this process. Volatility harvesting requires assets that move imperfectly together. When correlations are low or unstable, price dispersion creates repeated opportunities to reset portfolio weights. These resets convert relative price movement into incremental growth. Over time, the portfolio accumulates more units of assets that oscillate, improving geometric (compound) returns relative to a static buy-and-hold allocation. This is why diversified portfolios often outperform their components despite holding no superior assets.

The most robust way to understand rebalancing is as a controlled Markov process. At any moment, the state of the system is defined by prices, weights, and distance from target allocations. The investor controls the system by choosing when and how much to rebalance. The objective is to maximise long-run log growth — the same criterion underlying Kelly-optimal strategies — subject to transaction costs and liquidity constraints. Continuous rebalancing is inefficient; never rebalancing leaves convexity unharvested. Optimal portfolios therefore rebalance discretely to maintain allocation weights in banded ranges and trade only when the expected convexity gain exceeds frictional costs. Volatility harvesting is not a heuristic. It is a growth optimisation problem under uncertainty.

Well-designed portfolios do not fear volatility. They are built to use it.

Keywords: Volatility Harvesting, Portfolio Convexity, Rebalancing Strategies, Correlation, Long-Term Compounding, Log Growth, Stochastic Control, Macro Pairs Trading, Quantitative Portfolio Management, Growth-Optimal Investing

Recommended Reading:

IBKR Quant Campus:

Quantitative finance articles and programming tutorials. The IBKR Quant Blog serves quantitative professionals who have an interest in programming. Discussion topics include deep learning, IBKR API, artificial intelligence (AI), Python, R, C#, Java and more.

Bonus Article: A Real-World Illustration: Volatility Harvesting Through Systematic Portfolio Rebalancing

Consider a simplified, real-world portfolio structured for robust long-term growth. It has two sleeves:

Macro sleeve — allocates across UK Gilts, global equities, and physical gold.

ETF sleeve — holds diversified equity ETFs combining USD-denominated and GBP-denominated exposure, embedding both equity and FX volatility.

Rebalancing occurs within the ETF sleeve (capturing combined equity and FX volatility) and at the macro level between equities, bonds, and gold, responding to relative performance rather than predicting markets.

The portfolio starts at £1,000,000 with allocations of 50% equities (£500k), 40% Gilts (£400k), and 10% gold (£100k). Over the first six months, equities rally 20%, Gilts fall 5%, and gold remains flat. A systematic rebalance to preserve allocation weights trims equities and reallocates to bonds and gold. Six months later, markets reverse: equities fall 15%, Gilts rally 8%, and gold rises 5%.

After this period, the portfolio’s total value is £1,096,500 with systematic rebalancing, compared to £1,086,000 under a buy-and-hold approach. The incremental benefit of £10,500 comes purely from capturing volatility via rebalancing.

Explicit Benefit of Rebalancing:

Buy-and-hold value: £1,086,000

Rebalanced value: £1,096,500

Incremental growth from volatility harvesting: £10,500

This illustrates that systematic rebalancing accumulates more units of underperforming assets while trimming the overperforming ones, leading to higher compounded portfolio growth without leverage or forecasting.

Keywords: Volatility Harvesting Example, Systematic Rebalancing, Portfolio Convexity, ETF Portfolio Management, FX Volatility, Macro Asset Allocation, Long-Term Compounding, Units Accumulation, Macro Pairs Trading

Exclusive Algo Quant Store Discounts

Algo Trading & Quant Research Hub

Get 25% off all purchases at the Algo Quant Store with code 3NBN75MFEA.

Useful Links

Quant Research

SSRN Research Papers - https://ssrn.com/author=1728976

GitHub Quant Research - https://github.com/nburgessx/QuantResearch

Learn about Financial Markets

Subscribe to my Quant YouTube Channel - https://youtube.com/@AlgoQuantHub

Quant Training & Software - https://payhip.com/AlgoQuantHub

Follow me on Linked-In - https://www.linkedin.com/in/nburgessx/

Explore my Quant Website - https://nicholasburgess.co.uk/

My Quant Book, Low Latency IR Markets - https://github.com/nburgessx/SwapsBook

AlgoQuantHub Newsletters

The Edge

The ‘AQH Weekly Edge’ newsletter for cutting edge algo trading and quant research.

https://bit.ly/AlgoQuantHubEdge

The Deep Dive

Dive deeper into the world of algo trading and quant research with a focus on getting things done for real, includes video content, digital downloads, courses and more.

https://bit.ly/AlgoQuantHubDeepDive

|  |

Feedback & Requests

I’d love your feedback to help shape future content to best serve your needs. You can reach me at [email protected]