- AQH Weekly Deep Dive

- Posts

- Quantlab by Algorithmica: The Fastest Quant Stack in the World

Quantlab by Algorithmica: The Fastest Quant Stack in the World

AlgoQuantHub Weekly Deep Dive

Nicholas Burgess

March 20, 2026

Welcome to the Deep Dive!

Each week on The Deep Dive we explore cutting-edge ideas in algorithmic trading, quantitative research, and modern financial engineering.

This week, I was in Stockholm, Sweden to try out the world’s fastest low-latency infrastructure for trading and Quants. This week’s feature article discusses how in modern quantitative finance true competitive edge is no longer just model sophistication, but the ability to compress the entire lifecycle from research to production into hours rather than months by unifying pricing, risk, and market data within a single, real-time, low-latency infrastructure.

Bonus content, this week we show how Quantlab transforms the traditional multi-layered development pipeline into a single, unified workflow where models can be built, calibrated, and deployed in real time with consistent pricing and risk outputs across trading systems.

Table of Contents

Feature Article: The Fastest Quant Stack in the World — From Idea to Production in Hours, Not Months

For decades, quantitative finance has relied on fragmented architectures: separate systems for market data, pricing libraries, risk engines, and trading infrastructure. While powerful, these stacks introduce a fundamental constraint—time-to-market. Building and deploying new pricing models or structured products often requires weeks or months of engineering effort, creating friction between research and production. In fast-moving markets, this delay becomes a structural inefficiency, not just an operational inconvenience.

This is where Algorithmica’s Quantlab stands apart. Rather than competing with existing infrastructure, Quantlab is designed to collaborate seamlessly with it. It can sit alongside legacy systems, complement existing codebases, or fully replace them where needed. Institutions can host their own models within Quantlab, embed Quantlab inside their internal architecture, or adopt a hybrid approach—creating a flexible integration layer rather than a rigid dependency. This modularity is critical in real-world environments where ripping out legacy systems is often impossible.

What truly differentiates Quantlab is its ability to unify market data, pricing, and risk in real time within a single framework. The platform’s real-time evaluation engine allows users to ingest live data, perform analytics, and distribute results across systems instantly . This ensures that all users—across desks, asset classes, and systems—are working off the same consistent pricing and risk outputs. In practice, this eliminates both user arbitrage (inconsistent valuations across desks) and cross-asset arbitrage (misaligned models or data between asset classes) by keeping market data and models synchronised continuously. Combined with its ultra-low latency architecture and extensive quantitative library, Quantlab enables quants to move from idea to production in hours, fundamentally changing how modern quant teams operate.

Resources:

Keywords: QuantLab, Algorithmica, rapid development, real-time pricing, real-time risk, quant infrastructure, low latency pricing, real-time risk, time to market, derivatives analytics, cross-asset consistency, market data integration, quant platforms

Bonus Article:

Implementing Resilient Risk Management in Practice

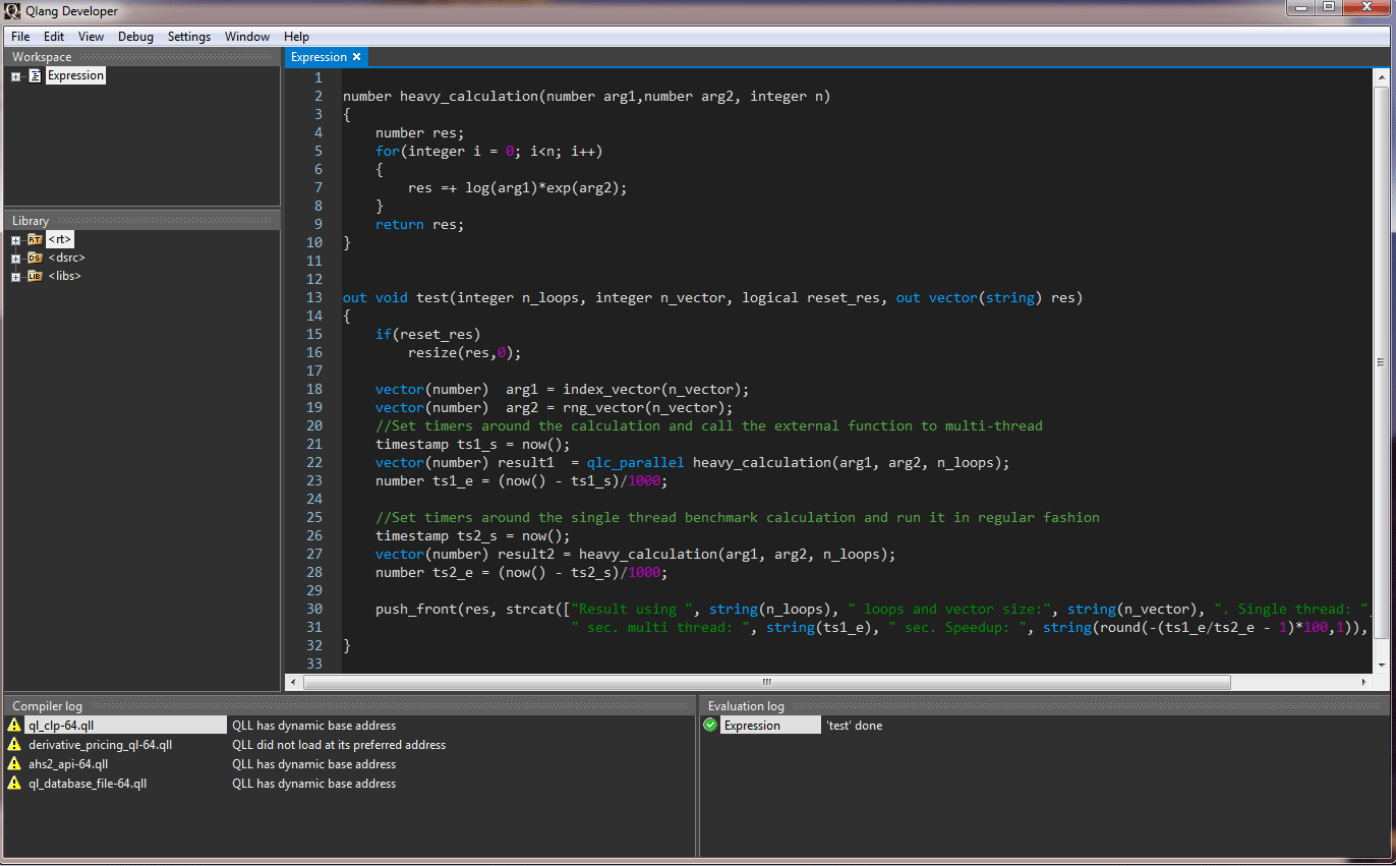

The practical impact of a platform like Quantlab is best understood through workflow. In a traditional setup, implementing something like a new credit derivative or exotic payoff requires coordination across multiple layers: model design in Python, translation into C++, integration with pricing libraries, testing, and eventual deployment. Each step introduces friction, delays, and potential inconsistencies between research and production environments.

With Quantlab, this pipeline is radically simplified. A quant can define a model, calibrate it, and generate pricing and risk outputs within a single environment—without rewriting logic across languages or systems. Because the platform is built for performance from the outset, the same code used for prototyping can operate at production-level speed. This eliminates one of the biggest inefficiencies in quant development: the disconnect between what works in research and what actually gets deployed. The result is a workflow where innovation is limited only by your imagination—not infrastructure.

A simple but powerful example of Quantlab in practice is its integration into electronic trading workflows. Through its partnership with TransFICC, Quantlab is used as a real-time pricing engine for swap RFQs (Request-for-Quote). In this setup, Quantlab is embedded directly into an existing trading platform, providing ultra-fast pricing and analytics without requiring firms to rebuild their infrastructure from scratch . This demonstrates the platform’s core philosophy: augment, don’t replace—unless you want to.

From an implementation perspective, the workflow is radically simplified. Market data is ingested, models are evaluated in real time, and pricing outputs are immediately available to trading systems and users. Because the same engine handles both analytics and distribution, results can be shared across desks or external systems with minimal overhead. This removes the traditional need to reconcile outputs across multiple libraries or environments. The result is a consistent, low-latency pipeline where pricing, risk, and trading decisions are all driven from a single, synchronised source of truth—exactly what modern quant desks need to operate efficiently and competitively.

Keywords: Quantlab workflow, rapid prototyping, quant development, derivatives implementation, low latency trading, pricing systems, risk systems, quant productivity, Quantlab implementation, swap pricing engine, real-time analytics, RFQ pricing, low latency trading, quant workflows, market data integration, pricing consistency

Algo Quant YouTube Channel

Algo Trading & Quant Research Channel YouTube playlists include:

Interest Rate Markets

Bond Markets

Credit Derivatives

Monte Carlo Simulation

Advanced Quant Models

American Option Trading

Live Algo Trading with IB Broker

Useful Links

Quant Research

SSRN Research Papers - https://ssrn.com/author=1728976

GitHub Quant Research - https://github.com/nburgessx/QuantResearch

Learn about Financial Markets

Subscribe to my Quant YouTube Channel - https://youtube.com/@AlgoQuantHub

Quant Training & Software - https://payhip.com/AlgoQuantHub

Follow me on Linked-In - https://www.linkedin.com/in/nburgessx/

Explore my Quant Website - https://nicholasburgess.co.uk/

My Quant Book, Low Latency IR Markets - https://github.com/nburgessx/SwapsBook

AlgoQuantHub Newsletters

The Edge

The ‘AQH Weekly Edge’ newsletter for cutting edge algo trading and quant research.

https://bit.ly/AlgoQuantHubEdge

The Deep Dive

Dive deeper into the world of algo trading and quant research with a focus on getting things done for real, includes video content, digital downloads, courses and more.

https://bit.ly/AlgoQuantHubDeepDive

|  |

Feedback & Requests

I’d love your feedback to help shape future content to best serve your needs. You can reach me at [email protected]