- AQH Weekly Deep Dive

- Posts

- Cross Currency Basis Arbitrage & Relative Value Trading

Cross Currency Basis Arbitrage & Relative Value Trading

AlgoQuantHub Weekly Deep Dive

Nicholas Burgess

July 04, 2025

Welcome

Welcome to AlgoQuantHub’s Weekly Deep Dive into Algo Trading & Quant Research!

AlgoQuantHub includes the latest hands-on quant tutorials, videos and research, helping you bridge the gap between theory and real-world quant practice. All delivered by this newsletter! Each week I will deliver a targeted deep dive into a feature topic.

Last weeks’ feature article explored how quantitative research gives traders a real edge in Bond Futures Cash Basis Trading Strategies—especially when leverage and embedded options come into play.

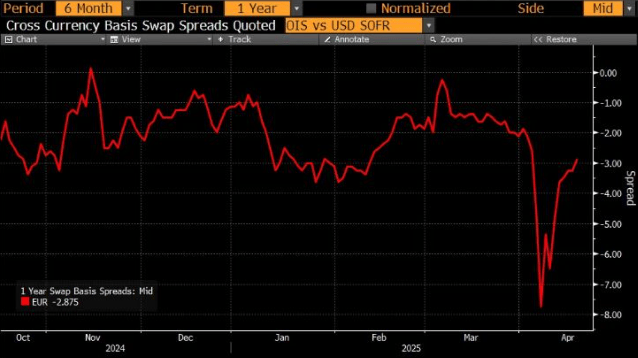

This week we look at Cross Currency Basis Arbitrage & Relative Value Trading. We explain the drivers of the basis including liquidity and market microstructure, and consider potential trading strategies.

Table of Contents

Digital Download Discounts

In this week’s newsletter we give readers a digital download discounts for use in AlgoQuantHub’s digital download store https://payhip.com/AlgoQuantHub

25% off IR & Fixed Income Training Bundle

Code: 8BWNUZTJUS

20% off total order amount

Code: GKJ1Y95OVR

Feature Article - Currency Basis Arbitrage and Relative Value Trading

Background Reading

Interest Rate Parity & Synthetic FX Forward Explained

For decades, global financial markets have relied on the seamless flow of capital across borders. But beneath the surface of currency exchange lies a crucial yet often overlooked mechanism: the cross-currency basis. This spread, which reflects the cost of swapping one currency for another via the short-term funding markets, serves as a barometer of global liquidity, central bank policies, and financial system stress.

At its core, the cross-currency basis represents the difference between the implied interest rate from FX swaps and standard interbank rates. In theory, arbitrage should keep this spread near zero, but in reality, it fluctuates due to market imbalances, funding pressures, and shifts in monetary policy. These distortions create opportunities for sophisticated traders (banks, hedge funds, and asset managers) who exploit the basis for arbitrage, hedging, and macro positioning.

This primer runs through:

Cross-Currency (XCCY) Basis Swaps

Key Participants in the Market

Drivers of XCCY Basis Movements

Liquidity and Market Structure

Trading Strategies

Behavioural Aspects and Market Psychology

Full Article - Global Primer Series: Cross Currency Basis

https://www.alphapicks.co.uk/p/global-primer-series-cross-currency?utm_source=algoquanthub.beehiiv.com&utm_medium=referral&utm_campaign=algoquanthub-weekly-deep-dive

Xccy Basis EUR/USD

Further Reading

CME Group: How U.S.-EU Relations Could Impact the Cross Currency Basis

Number Analytics: The Final Guide to Cross Currency Basis Explained

Number Analytics: A Quick Guide to Cross Currency Basis Simplified

Clarus FT: Cross Currency Swaps Review 2024

AlphaPicks: Global Primer Series: Cross Currency Basis

CME Group: Understanding EUR/USD Cross-Currency Basis Futures

Frontier Advisors: Cross currency basis swaps

Feature Video - Quant YouTube Channel

Subscribe to AlgoQuantHub’s Quant YouTube Channel!

Algorithmic Trading & Quant Research Hub or AlgoQuantHub for short is your go-to destination for in-depth insights into quantitative finance, algorithmic trading strategies, and advanced financial engineering. This channel delivers expert-led tutorials and research-driven content on topics such as bond pricing, yield curves, total return swaps, credit default swaps, and market microstructure, tailored for both aspiring and experienced quants. Whether you're looking to unlock quant models, master electronic market dynamics, or explore the latest in statistical arbitrage and trading automation, you'll find practical guides, detailed explanations, and actionable strategies to help you excel in the fast-paced world of modern finance.

Feature Download - Interest Rate Markets Training Bundle

Visit AlgoQuantHub’s Digital Download Store!

This week we feature the Interest Rate Markets Training Bundle, which contains Excel workbooks, PowerPoint and PDF training materials for interest rate and fixed income markets including the following,

Overview of Interest Rate Markets

Interest Rate Swaps

Cross Currency Swaps

Credit Default Swaps

Quanto Credit Default Swaps

This bundle includes a detailed overview of Interest Rate Markets, plus example workbooks and documentation for Interest Rate Swaps, Cross Currency Swaps, Credit Default Swaps, and Quanto Credit Default Swaps. A practical set of resources to build your understanding of key interest rate and credit derivatives.

Click on the image below for more info!

Feature Book - Machine Learning for Algorithmic Trading

The explosive growth of digital data has boosted the demand for expertise in trading strategies that use machine learning (ML) and the use of sophisticated supervised, unsupervised, and reinforcement learning models.

This book introduces end-to-end machine learning for the trading workflow, from the idea and feature engineering to model optimization, strategy design, and backtesting. It illustrates this by using examples ranging from linear models and tree-based ensembles to deep-learning techniques from cutting edge research.

Click on the image below for more info!

Useful Links

Quant Research

Links to my Quant Research

SSRN Research Papers

https://ssrn.com/author=1728976

GitHub Quant Research

https://github.com/nburgessx/QuantResearch

Learn about Financial Markets

Linked to learning resources for Financial Markets

Subscribe to my Quant YouTube Channel

https://youtube.com/@AlgoQuantHub

Algorithmic Trading & Quant Research Hub

https://payhip.com/AlgoQuantHub

Follow me on Linked-In

https://www.linkedin.com/in/nburgessx/

Explore my Quant Website

https://nicholasburgess.co.uk/

Read my Quant Book - Low Latency IR Markets

https://github.com/nburgessx/SwapsBook

AlgoQuantHub Newsletters

My AlgoQuantHub (AQH) newsletters showcase the latest hands-on quant tutorials, videos and research, helping you bridge the gap between theory and real-world quant practice.

The Edge

The ‘AQH Weekly Edge’ newsletter for cutting edge algo trading and quant research.

https://bit.ly/AlgoQuantHubEdge

The Deep Dive

In this newsletter we deep dive into the world of algo trading and quant research with a focus on implementation and getting things done for real, and includes video content, digital downloads, courses and more.

https://bit.ly/AlgoQuantHubDeepDive

|  |

Feedback & Requests

I’d love your feedback to help shape future content to best serve your needs. You can reach me at [email protected]